Author:

Judith Burson, CA

DM Gibson Accountants Limited

E: [email protected]

Edited by:

Integra International

Grant Gilmour, B.Sc., MBA, CA, CPA Canada, BC, CPA USA, Az, GDipICL.Sc.

INTEGRA TAX WORLD NEWSLETTER EDITOR

E: [email protected]

New Zealand’s R&D tax credit regime

Summary

In the past couple years there have been several changes to the mechanism to apply for R&D tax credit regime. The most significant is that previously applications for R&D was handled through a commercial entity via a grant mechanism, however it is now handled by the New Zealand Inland Revenue Department using the R&D Tax Incentives.

The R&D tax credit regime is designed to encourage business-led innovation by providing a refundable tax credit or cash out for qualifying expenditure, with strict eligibility criteria and caps on foreign research.

Claimants must comply with filing and record-keeping requirements, and certain exclusions apply to prevent double-dipping or subsidised expenditure.

The R&D tax credit regime provides a 15% tax credit for eligible research and development expenditure, with the aim of incentivising business innovation and increasing domestic R&D activity.

Eligibility Criteria

A critical part of the definition of an R&D activity is the requirement that it must seek to resolve scientific or technological uncertainty.

You must be trying to do something that a competent professional in that field is uncertain can be done. If others have successfully done what you are trying to do, your work will not be eligible for the tax credit – unless the knowledge of how to do it was still a trade secret.

The test is not that no-one in your business knows how to achieve your goal, or no one in New Zealand has done it before, but that the knowledge is not publicly available in the world. You must be able to show that you searched for an existing solution before you started your R&D activity.

Eligibility Criteria:

- The claimant must carry on business through a fixed establishment in New Zealand and perform core R&D activities in New Zealand.

- Eligible entities include private sector businesses, sole traders, partnerships, companies, joint ventures, and trusts. Crown research institutes, district health boards, tertiary education organisations, and their associates are excluded.

- The minimum eligible expenditure threshold is $50,000 per income year, unless using an approved research provider.

- The claimant must not receive any other R&D grants e.g. the Callaghan Innovation Growth grant (a specific program available in New Zealand).

- The claimant must own or have the right to use the results of the R&D activities.

Foreign and NZ-Based Research:

- R&D conducted overseas is eligible only if it is integral to a project based in New Zealand and is capped at 10% of total eligible expenditure incurred in New Zealand.

- Stand-alone overseas R&D is not eligible for the tax credit as only NZ taxpayers can claim a credit.

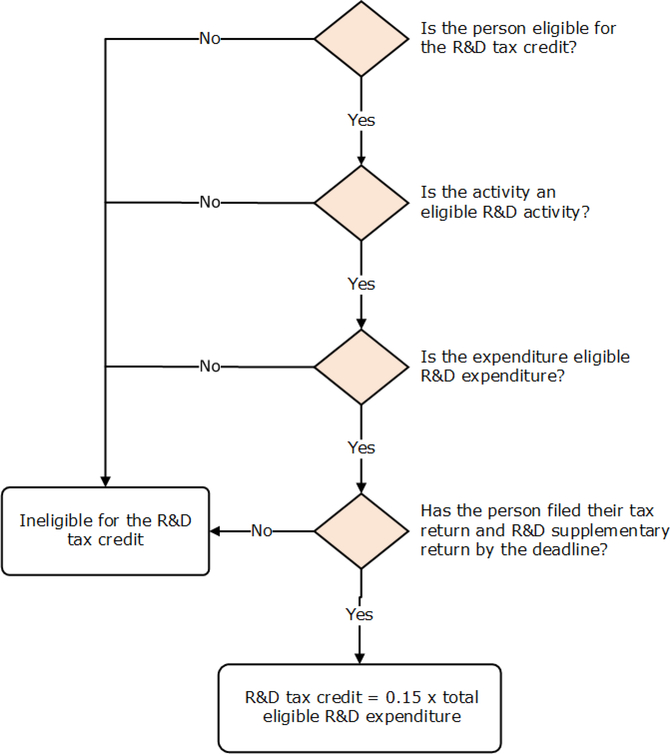

Quick overview of eligibility

The flowchart below provides a quick overview of eligibility requirements for the tax credit.

Eligible Expenditure:

- Includes employee remuneration, training, travel, depreciation of tangible property, consumables, certain overheads, and payments to entities conducting R&D on behalf of the claimant.

- Excludes expenditure funded by government grants, co-funding, and expenditure for which a tax credit has been received in another country.

- Excludes expenditure not directly attributable to R&D activities such as the general operating expenses, professional fees, office rental, interest expenditure etc.

Issues, Limitations and Exclusions

Expenditure funded by government grants or for which a foreign tax credit has been claimed is not eligible.

The regime focuses on where the R&D is performed, not where the intellectual property is held. (see Claw Backs regarding the “cash out” regime).

Certain activities (e.g., market research, social sciences, arts, humanities, prospecting, and quality control) are expressly excluded from eligibility.

Expenditure Limits and Exclusions

Key limits and exclusions include:

- Activities performed outside New Zealand, unless they are integral to a core R&D activity conducted in New Zealand and subject to a 10% cap of total eligible expenditure.

- Acquisition or disposal of land, except where land is used exclusively for housing R&D facilities.

- Acquisition, disposal, or transfer of intangible property (other than software), core technology, intellectual property, or know-how, and related activities.

- Prospecting, exploring, or drilling for minerals, petroleum, natural gas, or geothermal energy.

- Research in social sciences, arts, or humanities.

- Market research, market testing, market development, or sales promotion, including consumer surveys.

- Quality control, routine testing, routine collection of information, and routine operations on data.

- Expenditure for patenting and complying with statutory requirements and standards.

- Pre-production activities, reverse engineering, minor adaptations, cosmetic or stylistic changes, and routine software testing, debugging, maintenance, and conversion.

- Expenditure to commercialise the results of R&D, including preproduction expenditure.

- Gifts, interest, royalties, and expenditure above market value for goods and services.

- Expenditure for which a foreign country provides a similar R&D tax credit.

- Internal software development is subject to a cap (currently $25 million).

These limits and exclusions are intended to ensure that only genuine, innovative R&D activities and related costs qualify for tax incentives.

R&D Claw backs

Claw backs related to R&D expenditure primarily arise in the context of the R&D tax loss “cash out” regime. This regime allows eligible start-up companies to receive a refundable tax credit for tax losses arising from qualifying R&D expenditure, rather than carrying the loss forward. However, claw backs occur if the company subsequently earns assessable income or makes a successful return on its investment through a non-taxable capital gain. In such cases, the value of the cashed-out loss must be repaid, either through taxes paid on future income or by reinstating the cashed-out losses as losses to carry forward and repaying the value out of the gain made.

Triggers for early repayment (claw back) include:

- Sale of R&D assets

- Ceasing to carry on business

- Change in company ownership or structure

- Making a successful return on investment through capital gains [NZ currently has no capital gain tax].

These claw backs are intended to ensure that the cash-out regime provides only a timing benefit, not a permanent subsidy, and that companies repay the government support if they become profitable or realise capital gains from their R&D activities.

Double Dipping Exclusions

Double dipping exclusions in the R&D tax incentive regime refer to rules that prevent claiming the same expenditure for tax credits in multiple jurisdictions or through multiple funding sources. Key exclusions include:

- Expenditure for which a person has received an R&D tax credit from another country is not eligible for the New Zealand R&D tax credit. This prevents double dipping by ensuring that the same expenditure cannot be claimed for tax credits in more than one country.

- Expenditure funded by a government or local authority grant is excluded. If a business receives a grant and spends it on what would otherwise be eligible R&D expenditure, that expenditure is ineligible for the tax credit. This also applies to co-funding arrangements where a business or third party contributes funds as a condition of obtaining a grant.

- Gifts used in R&D are not eligible for the tax credit, as only costs incurred for R&D activities are eligible. However, consideration for a service (such as a gift voucher given to a participant in a medical trial) is eligible.

- Expenditure which is eligible expenditure of someone else is excluded, ensuring that only the entity incurring the cost can claim the credit.

These exclusions are designed to ensure the integrity of the R&D tax incentive regime and prevent multiple claims on the same expenditure, whether across jurisdictions or funding sources.

Claim Back Mechanism:

- The tax credit is claimed in the annual income tax return, offsetting the tax liability of the claimant.

- Surplus credits are refundable, meaning businesses in a tax loss position or with only tax-exempt income can receive the credits in cash.

- Claimants must file both their income tax return and an R&D supplementary return within 30 days of the latest filing due date.

- Claimants must file their income tax return within a year of the end of the tax year.

- Detailed statements of R&D activities and expenditure must be provided for administrative and evaluation purposes.

Evaluation and Transparency

The New Zealand Inland Revenue publishes the names and amounts of R&D tax credits claimed (in dollar bands) two years after the tax year.

The R&D regime is independently evaluated every five years.

Conclusion

New Zealand’s R&D tax credit regime provides a 15% incentive to support business‑led innovation, but eligibility is tightly defined. Claimants must demonstrate genuine scientific or technological uncertainty, meet strict New Zealand‑based activity requirements, and avoid double‑dipping with grants or foreign tax credits. Expenditure limits, exclusions, and claw back rules ensure the regime targets true R&D rather than routine or commercial activities. Overall, the system offers meaningful support for innovation while maintaining strong integrity and compliance controls.

Disclaimer

This communication contains general information only based on collective research. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No representations, warranties or undertakings (express or implied) are given as to the accuracy or completeness of the information in this communication, and none of DM Gibson Accountants Limited, Integra International, related entities, employees or agents shall be liable or responsible for any loss or damage whatsoever arising directly or indirectly in connection with any person relying on this communication.

DM Gibson Accountants Limited and Integra International, and their related entities, are legally separate and independent entities.

Copyright

© 2026 Integra and DM Gibson Accountants Limited

About the Author:

Judith Burson, CA

Judith Burson, CA is Senior Manager. She has been a CA for 21 years and specializes in the taxation of private companies and family trusts.

About the member firm:

At DM Gibson Accountants Limited we are dedicated to bringing you the highest quality professional service and guidance. Our accountants can help you in a wide range of areas and being fluent in English and Mandarin will ensure that nothing gets lost in the detail.

What sets DM Gibson Accountants Ltd apart from most accounting firms is that we provide all the services required to run a successful business.

Don Gibson has 41 years of experience in the public practice industry and has built up an extensive network of professional specialists in New Zealand and overseas. This network is used to provide specialised services to our clients to ensure that, in a nutshell, we are a ‘one stop business shop’.

Rachel Sargent has honed her business services and advisory expertise over the last 19 years to ensure that our services stay relevant for our clients’ needs.

Integra Profile

https://integra-international.net/find-an-integra-firm/find-firm-profile/name/dm-gibson-accountants-ltd/

Member website

https://www.gibsonca.co.nz/