Author:

Rakesh Ghirah

Londen & Van Holland, Partner

E: [email protected]

Ismail Agarmis

Londen & Van Holland, Senior Manager VAT (Indirect Tax)

E: [email protected]

Edited by:

Integra International

Grant Gilmour, B.Sc., MBA, CA, CPA Canada, BC, CPA USA, Az, GDipICL.Sc.

INTEGRA TAX WORLD NEWSLETTER EDITOR

E: [email protected]

E-invoicing & VAT Developments in the Netherlands

This presentation covers the regulatory framework, implementation timeline, and technical specifications for electronic invoicing in the Netherlands, highlighting recent developments and future mandates.

Under Article 35d of the Dutch VAT Act, implementing Article 233 of the VAT Directive, electronic invoices are legally equivalent to paper invoices provided authenticity of origin, integrity of content, and legibility are ensured. This reflects the EU principle of functional equivalence, meaning that legal validity depends on compliance characteristics rather than form.

Dutch law also embodies the principle of technology neutrality, allowing taxable persons to choose any technical solution that ensures compliance with these core principles. Historically, electronic invoicing in the Netherlands has therefore been based on voluntary adoption and contractual consent models.

In the Netherlands, B2G e‑invoicing has been partially mandatory since 2017, using UBL/SI‑UBL formats via Peppol and Digipoort. B2B e‑invoicing is currently voluntary but will become mandatory for qualifying transactions under ViDA from 2030. B2C invoicing remains outside mandatory scope

Technical Specifications & Implementation

Technically, the Dutch implementation model reflects the European interoperability architecture, with ERP systems generating structured invoices, transmission via Peppol access points, routing and validation through the Peppol network, and receipt by compliant recipient systems. Compliance is ensured through EN 16931 core elements and national CIUS specifications such as NLCIUS for B2G invoicing. These national subsets are legally permissible within the EN 16931 framework and serve to address specific public sector control requirements without undermining EU-wide interoperability. Identification mechanisms (KVK, VAT ID, OIN) create legally reliable entity authentication.

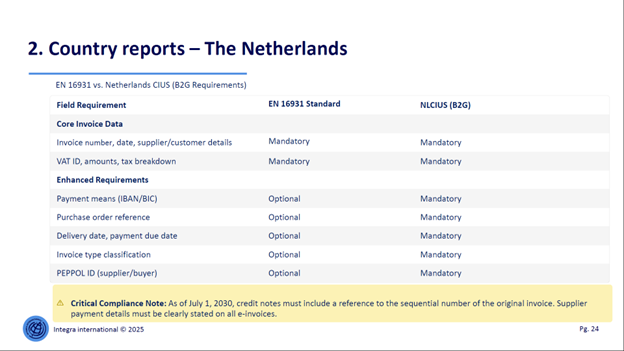

EN 16931 vs. Netherlands CIUS (B2G Requirements)

The Netherlands CIUS (NLCIUS) represents a legally permissible national specification within the EN 16931 framework, allowing additional public‑sector requirements without violating EU harmonisation rules.

National Roadmap

The Dutch roadmap follows the ViDA structure: policy development, legislative transposition, infrastructure development, and mandatory enforcement from July 2030. This ensures full legal and technical alignment with EU digital VAT architecture.

Disclaimer

This communication contains general information only based on collective research. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No representations, warranties or undertakings (express or implied) are given as to the accuracy or completeness of the information in this communication, and none of Londen & Van Holland, Integra International, related entities, employees or agents shall be liable or responsible for any loss or damage whatsoever arising directly or indirectly in connection with any person relying on this communication.

Londen & Van Holland and Integra International, and their related entities, are legally separate and independent entities.

© 2026 Integra and Londen & Van Holland

About the Author:

Rakesh Ghirah

Rakesh Ghirah is a Partner in the Indirect Tax practice at Londen & Van Holland, where he oversees and advises on complex VAT (Value Added Tax) and RETT (Real Estate Transfer Tax) matters for a broad portfolio of clients ranging from medium‑sized enterprises to large multinational organizations. His role includes providing strategic tax guidance, delivering specialised VAT trainings, and contributing to the further growth, innovation, and multidisciplinary collaboration within the firm’s tax practice.

Rakesh brings extensive experience gained from previous positions at the Dutch Tax Authorities, a top‑10 accounting firm, a Big Four organisation, and the Dutch Ministry of Finance, where he specialised in VAT policy and advisory work. His broad background enables him to combine deep technical knowledge with practical insight, supporting clients in navigating both domestic and international indirect tax challenges.

In addition to his professional advisory work, Rakesh is active in academia. He serves as Programme Coordinator for the Post‑Master Indirect Tax and Seminar Coordinator for the Top‑Level Seminar EU VAT at Erasmus Fiscal Studies. He is also a thesis supervisor at the Law & Tax department of Erasmus University Rotterdam, where he guides graduate students through advanced research in indirect taxation.

Rakesh also has significant experience in designing and implementing tax control frameworks, helping organisations strengthen their tax governance, manage risks, and align with regulatory expectations.

Through his combined practical, academic, and policy background, Rakesh plays a key role in shaping the future of the Indirect Tax practice at Londen & Van Holland and contributing to thought leadership within the broader tax community.

Ismail Agarmis

Ismail Agarmis is a Senior Manager VAT (Indirect Tax) at Londen & Van Holland, advising businesses on complex national and cross‑border VAT matters and helping organizations optimize compliance, reduce risk, and unlock financial opportunities within indirect tax systems. He has extensive experience advising multinational and national companies across a wide range of sectors, including international trade, toll manufacturing, automotive, e‑commerce, petrochemicals, electronics, and other internationally oriented industries. In addition to his tax‑technical expertise, Ismail is specialized in tax technology, including VAT compliance automation, VAT mapping across various ERP systems, and the design of technology‑enabled indirect tax processes. He has previously worked as VAT specialist at Big 4 firms both in the Netherlands and various multinational firms.

About Londen & Van Holland:

Londen & Van Holland was established in 1994 – large enough to provide the range of services that would enable it to compete against the existing big four but, at the same time, small enough to give its staff space for personal development. The company has grown into a medium-sized organization with around 150 staff with clients ranging from independent companies to subsidiaries of international companies and non-profit organizations.

Integra International Bio:

https://integra-international.net/find-an-integra-firm/find-firm-profile/name/londen-van-holland/

Londen & Van Holland: