Author:

Stefanie Feiste

Steuerberaterin, Partner, Wagemann + Partner

Geschäftsführer bei W+P US tax services GmbH Steuerberatungsgesellschaft

E: [email protected]

Edited by:

Integra International

Grant Gilmour, B.Sc., MBA, CA, CPA Canada, BC, CPA USA, Az, GDipICL.Sc.

INTEGRA TAX WORLD NEWSLETTER EDITOR

E: [email protected]

E-Invoicing in Germany from 2025 – What Businesses Need to Know

From 1 January 2025, electronic invoicing (e-invoicing) did become mandatory for domestic B2B transactions subject to VAT in Germany. This reform implements EU requirements and lays the foundation for a fully digital VAT system.

This article provides an overview of the legal framework, formats, timelines and practical processes.

1. What Is an E-Invoice?

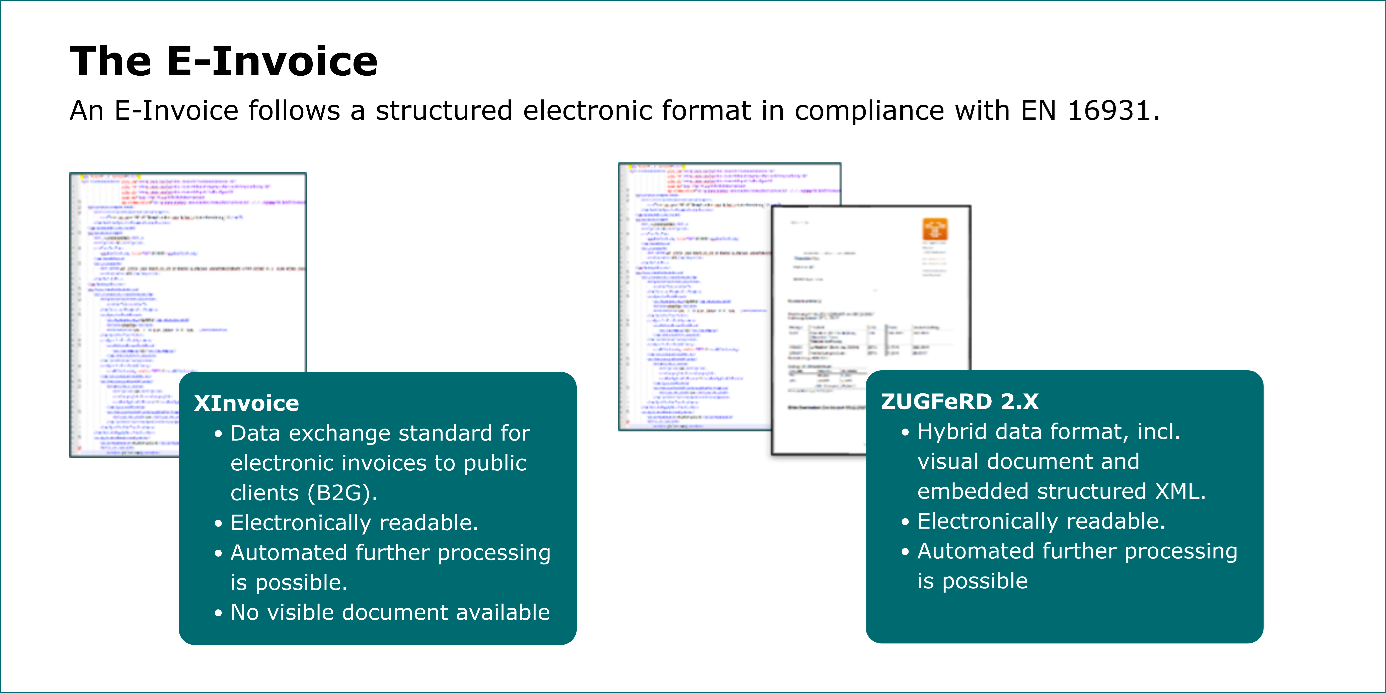

An e-invoice is not a simple PDF document sent by email. Instead, it must be issued in a structured electronic format compliant with EN 16931.

Common formats include:

- XInvoice

- Pure XML data format

- Fully machine-readable

- No visual representation

- Standard format for B2G transactions

- ZUGFeRD 2.x

- Hybrid format combining a PDF with embedded XML data

- Human-readable and machine-processable

- Widely used in B2B transactions

Only invoices in these formats qualify as legally valid e-invoices.

2. Legal Framework and Timeline

The obligation is based on an amendment to the German VAT Act.

Key points:

- From 01.01.2025: Mandatory e-invoicing for taxable domestic B2B transactions

- Transitional periods until the end of 2027

- Exceptions:

- Low-value invoices (< EUR 250)

- Tickets

From 01.01.2028 (planned): Introduction of a national VAT reporting system with mandatory data transmission via approved platforms

3. Who Is Affected?

In practice, almost all businesses operating in Germany are affected.

The obligation applies to B2B invoices issued by and to:

- Commercial enterprises

- Landlords

- Insurance companies

- Medical professionals and physicians

If a business is not technically able to receive e-invoices, the right to deduct input VAT may be denied under German VAT law. This makes implementation not only a legal, but also an economic necessity.

4. Transitional Rules for Issuing Invoices

During the transitional period:

- 2025–2026

- Paper invoices are still permitted

- Other electronic formats (e.g. PDF) may only be used with the recipient’s consent

- From 2027

- Businesses exceeding the EUR 800,000 turnover threshold must issue e-invoices

- Other businesses may still use alternative formats temporarily

From 2028 onwards, e-invoicing will become the standard for all domestic B2B transactions.

5. Invoice Issuance Deadline

According to § 14 para. 2 of the German VAT Act:

- E-invoices must generally be issued within six months after the supply of goods or services

- This applies in particular to:

- Supplies between entrepreneurs

- Taxable services related to real estate located in Germany

6. Special Rule for Continuous Obligations

For continuous obligations (e.g. rental agreements, long-term service contracts):

- It is sufficient to issue an e-invoice for the first billing period

- The underlying contract must be attached or clearly referenced

- This approach is confirmed by guidance issued by the German tax authorities

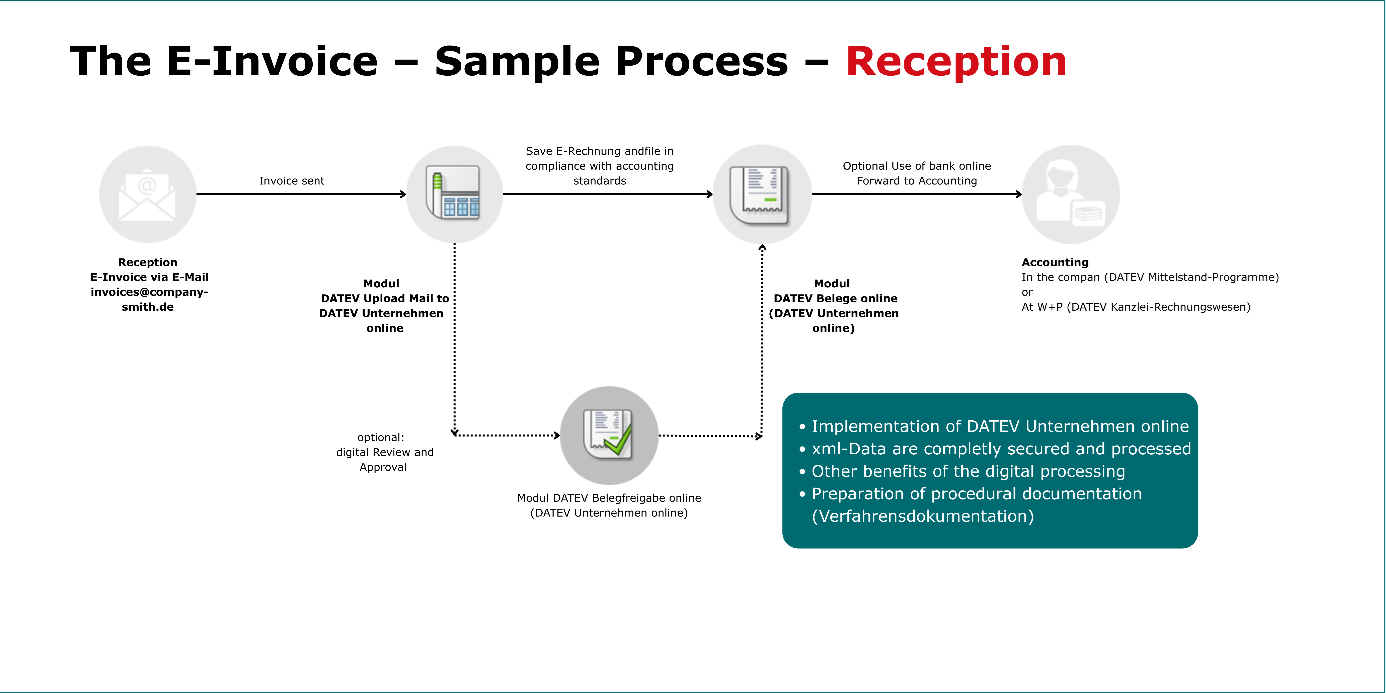

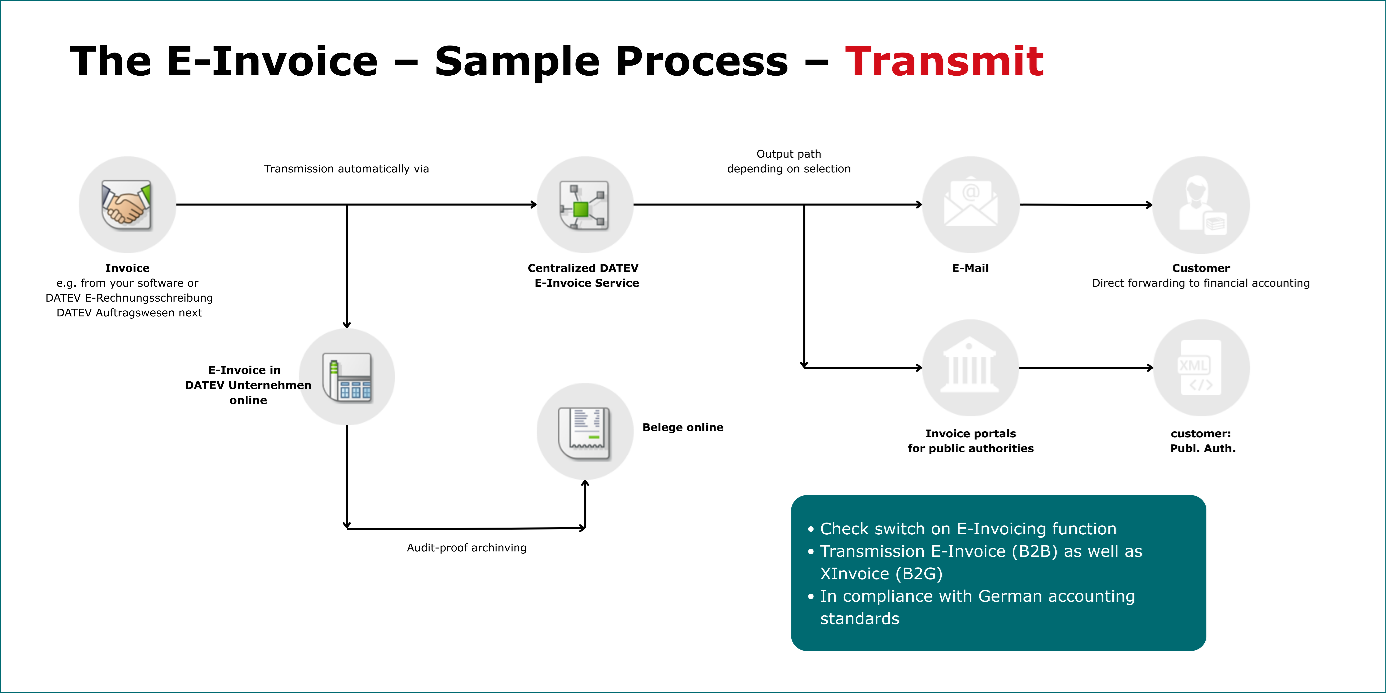

7. Example Digital Process (Inbound & Outbound)

Implementing e-invoicing goes far beyond the mere creation of invoices. It requires well-structured, secure and compliant digital processes that cover the entire invoice lifecycle.

A clear distinction is typically made between inbound and outbound processes:

Inbound:

- Receipt of e-invoice

- Automated upload and validation

- Digital approval

- Audit-proof archiving

- Transfer to accounting

Outbound:

- Creation via ERP or invoicing software

- Automatic transmission via email, platforms or public portals

- GoBD-compliant archiving

8. Conclusion

Germany’s e-invoicing framework introduces mandatory structured invoicing for B2B transactions in line with European standards. The phased implementation, standardized formats and interoperability requirements are designed to modernize invoicing processes and strengthen tax compliance.

E-invoicing is therefore not merely an IT topic, but a legal obligation with significant tax implications. Companies are well advised to act early in order to ensure compliance, increase efficiency and establish future-proof processes.

Disclaimer

This communication contains general information only based on collective research. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No representations, warranties or undertakings (express or implied) are given as to the accuracy or completeness of the information in this communication, and none of Wagemann + Partner, Integra International, related entities, employees or agents shall be liable or responsible for any loss or damage whatsoever arising directly or indirectly in connection with any person relying on this communication.

Wagemann + Partner and Integra International, and their related entities, are legally separate and independent entities.

© 2026 Integra and Wagemann + Partner

About the Author:

Stefanie Feiste

Stefanie Feiste has been part of Wagemann + Partner since 2008 and is a partner of the firm. She specializes in advising high-net-worth individuals and supports companies across a wide range of industries and legal structures. Her work also focuses on international tax law, particularly double taxation matters and tax issues with a U.S. connection.

She studied Baltic Management Studies at Stralsund University of Applied Sciences and earned a Bachelor of Business Administration in 2009, with all courses taught in English. Stefanie completed her training as a tax clerk in 2011 and was appointed as a tax advisor in May 2017.

Wagemann + Partner PartG mb :

Wagemann + Partner PartG mbB is a German tax consulting, auditing, and legal advisory firm with offices in Berlin, Düsseldorf, and Hamburg. For almost 50 years, we have been providing comprehensive advisory services in tax, audit, law, and business matters.

We offer extensive advice on all matters relating to German and international tax law, including double taxation treaties. Our clients include German individuals and companies with international activities, as well as foreign individuals and businesses operating in Germany.

As a member of INTEGRA INTERNATIONAL, an interactive global association of independent accounting and consulting firms, we are represented worldwide. Our personalized consulting services meet the highest professional standards of expertise and quality. We are committed to delivering creative and innovative solutions, supported by state-of-the-art technologies and modern communication and document management systems

Integra International Bio:

Wagemann + Partner: